MAPS: Fortifying the Record Before the Bid

After months of letters, videos, and public analysis, the remaining valuation questions are no longer public ones.

Disclosure: As of publication, I beneficially own well in excess of 1,000,000 shares of WM Technology, Inc.’s Class A common stock, inclusive of common stock underlying immediately exercisable derivative instruments. I have continued to increase that position materially since my February 23, 2026 notice to the Board, and I may buy or sell securities at any time without further notice. I am acting independently. This post reflects my personal opinions based solely on publicly available information. Full legal disclaimers appear at the end of this post.

I see probability-weighted standalone value materially above the recent sub-$1 tape, and I have spent the last two months building the public record to support that view.

This post is not the beginning of my work on WM Technology, Inc. (Nasdaq: MAPS 0.00%↑). It is the point at which that work reaches the natural limit of what an outside holder can do from the public file alone.

For readers who prefer the spoken overview first, this video summarizes the core valuation, process, and record-building points developed in the analysis below.

The full written analysis follows.

For readers who want the underlying record, my prior sanitized correspondence archive is compiled here:

It reflects the valuation, process, capital-allocation, and disclosure issues I had already placed on the record before the 10-K was filed. More importantly, it fixes the chronology. The through-line was straightforward: the early-February sequence of events appeared consistent not merely with routine housekeeping, but with process-positioning for a possible renewed affiliated bid. That inference was later reinforced, not created, by the Company’s March 5 addition of a third independent director.

The 10-K now fixes the year-end baseline. MAPS reported FY25 revenue of $174.7 million, adjusted EBITDA of $39.8 million, net income of $3.3 million, operating cash flow of $26.2 million, and year-end cash of $62.4 million.

Those figures are worth translating into the current tape. With 159.0 million Class A plus Class V economic units outstanding and $62.4 million of cash, every $0.10 of stock price represents roughly $15.9 million of equity value. At $0.70 / $0.80 / $0.90 / $1.00 per share, MAPS would be trading at an enterprise value of only about $49 million / $65 million / $81 million / $97 million — roughly 1.2x / 1.6x / 2.0x / 2.4x FY25 adjusted EBITDA, or about 1.9x / 2.5x / 3.1x / 3.7x FY25 operating cash flow.

Share-count note: Company materials sometimes show a simplified pro forma common-stock count assuming vested Class P units convert at 1:1. I do not use that figure as my operative denominator because those same materials state the units are not necessarily exchangeable 1:1 and, at the December 31, 2025 share price, would have converted into only 1,061,930 Class A shares. The 10-K is more precise still: Class P units are exchangeable only for Class A value net of a participation threshold. I therefore treat them as contingent, price-sensitive upside dilution, not as current full-value common equivalents.

That does not prove fair value by itself. It does, however, show how compressed the current tape is even before assigning any credit to normalized customer economics, regulatory de-risking, or a control-context valuation framework.

What the market is actually pricing

The market is pricing the quote.

It is pricing the Nasdaq bid-price clock. It is pricing lingering internal-control weakness concerns. It is pricing cannabis fatigue, a broader software derating that had little to do with MAPS specifically, and a micro-cap buyer universe that has materially shrunk. It is also pricing a stock whose recent tape has been shaped more by optics, liquidity, and procedural uncertainty than by any careful attempt to isolate control-context value.

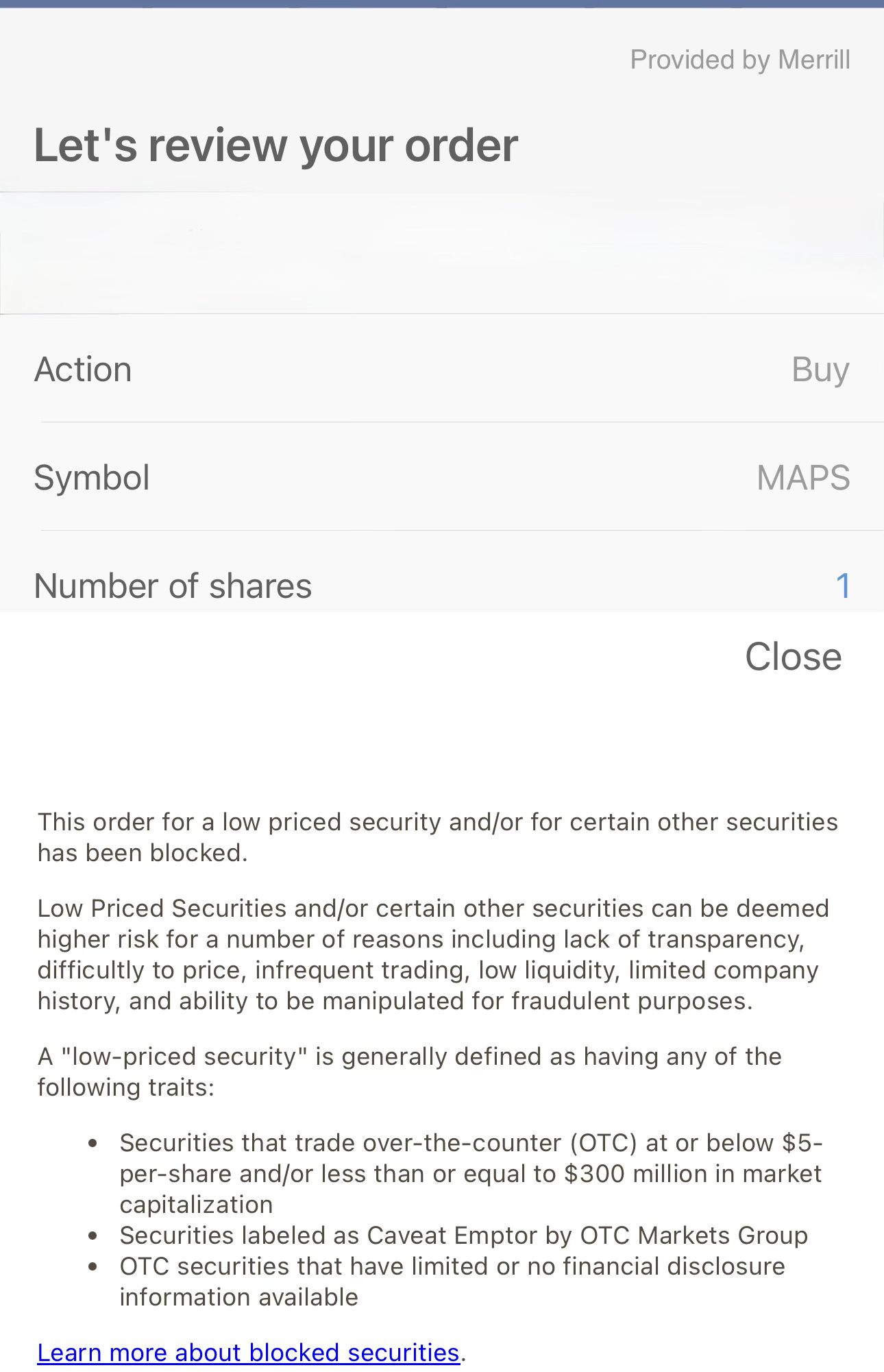

Retail access frictions may also be affecting the quote at the margin. On March 13, 2026, the day after the 10-K was filed, a Merrill retail account attempting to purchase MAPS received a low-priced-security block screen. I do not treat that single instance as dispositive. I do treat it as contemporaneous evidence that, at least at some firms or account configurations, the low-priced-security label may itself be narrowing the practical buyer universe and contributing to an affected tape.

That is a real setup.

But it is also not the same thing as intrinsic value.

An affected trading price can tell you plenty about the market’s tolerance for uncertainty. It does not, standing alone, tell you what a business is worth in a control context. That distinction becomes even more important where the Company has real cash, no funded long-term debt, and a valuation case that turns on what the business looks like once 280E goes away and the hemp loophole closes—not on whether the next quarter beats or misses by a million dollars.

In other words, the tape is a datapoint, not the verdict.

What my prior public record already established

None of this is post hoc.

Before the 10-K, I had already put the core valuation and process issues in writing to the Board and its advisors. The points were straightforward: any serious valuation exercise should use discrete bear/base/bull scenario analysis rather than a single-point exercise; it should guard explicitly against double counting risk across cash flows, discount rate, and terminal value; and it should reconcile unaffected and affected trading windows honestly in any affiliated-transaction context.

I also put a structural market-check problem squarely on the record. The founders’ prior proposal stated that a competing acquirer would face more than $100 million of incremental TRA cost at the proposed price, making competing bids “highly unlikely.” That matters because any later attempt to treat the absence of third-party interest as affirmative evidence of fairness would rest on a market check conducted in a structurally deterred environment. The Special Committee cannot credit that absence without first confronting the deterrent itself.

On capital allocation, I put a different but equally concrete issue on the record: “reverse split and hope” is not the only available response to a bid-price deficiency clock. Tender analysis, buyback analysis, cash-impact analysis, and real liquidity modeling are all part of the job. My February 9 proposal set out a specific, self-funded alternative. My February 12 notice then documented approximately $3.9 million of cumulative interest income forfeiture across FY2023 through 9M2025, a figure that ultimately exceeded the Company’s reported FY25 net income. That correspondence went by certified mail to the Board, the Audit Committee Chair, and Baker Tilly. I received no response.

Most importantly, I had already framed the incentive structure public holders should be watching. In December 2024, the co-founders submitted a non-binding proposal to acquire the Company for $1.70 per share. That proposal was later withdrawn in June 2025, but with an express reservation to return. That chronology is not background color. It is the frame through which the later sequence has to be assessed: a depressed quote, a deficiency clock, lingering litigation overhang, and then a governance pattern consistent with readiness for a possible renewed affiliated process.

That same public record also explains why my accumulation accelerated through February: valuation and process were pointing in the same direction. A broader software selloff, followed by the Nasdaq bid-price deficiency notice, compressed MAPS into a range that in my view bore little relationship to the economics of a debt-free, cash-rich, cash-generating platform business. At the same time, the early-February governance sequence — independent directors added, the CFO role made permanent, the deficiency clock triggered, and the class action settlement in principle surfacing on the public docket before the Company itself disclosed it — raised obvious questions about take-private readiness in a Company whose co-founders had already bid once, then withdrawn while expressly reserving the right to return. The subsequent March 5 addition of a third independent director was directionally consistent with that earlier pattern.

Those were not separate theories. They were parallel implications of the same evidence set: a dislocated quote and a governance pattern consistent with renewed affiliated-process optionality.

I am not backfilling a narrative after the fact. I am extending and fortifying a record I was already building.

What the 10-K does — and doesn’t — solve

One point should be confronted directly rather than massaged: the quarter itself was ugly. 4Q25 was loss-making. The filing also confirms that the Company’s internal control environment remains imperfect. Those are real facts. They are not, by themselves, a dispositive answer on intrinsic value.

What the 10-K does provide is a firmer and less avoidable public baseline.

Outside holders can now anchor the discussion to actual year-end numbers rather than inference: FY25 revenue of $174.7 million, adjusted EBITDA of $39.8 million, net income of $3.3 million, operating cash flow of $26.2 million, and year-end cash and cash equivalents of $62.4 million. On a Class A plus Class V economic-unit base of 159,040,266 as of March 5, 2026, that is roughly $0.39 of cash per share/economic unit.

Note: 19.5 million total warrants remain outstanding, all with an $11.50 exercise price and a June 16, 2026 expiration. At the current quote and under any realistic near-term affiliated-bid scenario, I treat them as non-economic and therefore exclude them from the operative valuation discussion.

Those datapoints matter because they narrow the honest standalone range. They are enough to reject lazy, tape-anchored valuation. They are not enough to answer the questions that would matter most in any renewed affiliated bid.

The filing still does not disclose management’s projections, the committee’s weighting of regulatory timing, the treatment of affected versus unaffected trading windows, or whether risk was layered into the valuation record once, twice, or three times through the combined use of cash-flow conservatism, discount-rate pressure, and terminal-value compression.

The 10-K is therefore both essential and insufficient: essential because outside holders should not skip the public work, and insufficient because the remaining decisive questions are no longer public-file questions.

FY25 also has a recognizable kitchen-sink character. Settlement accruals, contingencies, impairment charges, and other clean-up items all landed in the same year-end filing. That matters for optics. It does not relieve anyone of the obligation to distinguish bounded clean-up charges from normalized earnings power.

The point is not that the 10-K vindicates the tape. It does not. The point is that it narrows the range of honest disagreement while clarifying what still cannot be known from the outside.

That is precisely why I waited for it.

Having now waited for it, I think the public record is strong enough to reject superficial valuation, but still incomplete in exactly the places that would matter most in any renewed affiliated process.

The class action settlement is a required valuation input, not a narrative prop

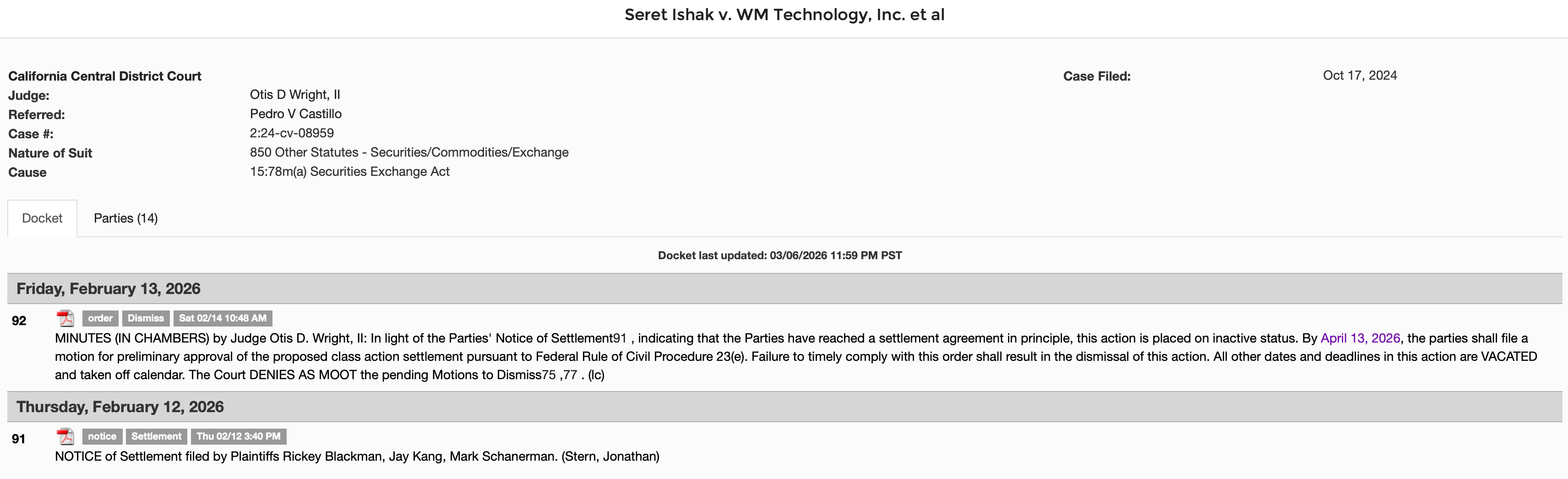

The class action settlement is a required valuation input, not a narrative prop. The 10-K discloses the economic contours of the Ishak securities class action settled in principle on February 12, 2026: the Company accrued $2.8 million representing its estimated portion of the outlay — just under $0.02 per Class A plus Class V share outstanding as of March 5, 2026. That is a real cost, just not a thesis-determinative impairment. Headline numbers are not valuation. Company cash exposure is. The settlement should be modeled, not mythologized. If filed terms materially alter the issuer-funded burden, payment timing, reserve treatment, insurance offset, or non-monetary provisions, those flow into the valuation bridge. On the current public record, this reads more like a process-clearing cost than a thesis-breaking hit to intrinsic value.

Preliminary approval motion is due April 13, 2026—that’s the next factual checkpoint. The consolidated derivative action (DeGennaro/Pearson v. Francis et al.) is a separate track, with that stay extended to April 10, 2026 to allow resolution discussions. Structurally, derivative claims assert harm on behalf of the Company. Net of D&O coverage and any litigation costs, any economic recovery would accrete back to the entity rather than dilute it. This is a governance and insurance matter, not an equity impairment event.

The most important modeling mistake: forcing a 2026 lens onto a 2028+ value problem

This is where I think the market is making its biggest error.

MAPS is being valued and viewed too narrowly through a 2026 lens when a large portion of its economic value sits in steady-state and beyond. That does not mean 2026 is irrelevant. It means a proper valuation should not allow temporary noise to dominate a business whose incremental value is driven by what normalized customer economics can look like after the regulatory transition period.

That is particularly true in a DCF framework.

If you build the model honestly, most of the value does not come from whether one quarter is ugly and kitchen-sinked, whether reporting and control issues cloud the near-term picture, or whether a deficiency notice compresses the holder base for a few months. Most of the value comes from what the business can earn once the cannabis industry’s most distortive pressures either ease or at least become more bounded and legible.

For MAPS, an overly near-term framing inherently understates value. Not because the near term is pretty. It is not. But because the near term is not where the bulk of the economics live.

The mistake isn’t simply conservatism.

It’s temporal myopia.

The first major variable is rescheduling and 280E relief

A serious valuation record cannot assign an implicit probability of zero to federal rescheduling and the resulting removal of Section 280E-related pressure on the Company’s customer base. This isn’t an abstract policy point. It’s a Company-specific valuation driver with a direct transmission mechanism into Weedmaps’ customer economics.

Today, the Company’s customers operate under a tax regime that is structurally punitive. Section 280E denies the deduction of ordinary business expenses for any business trafficking in Schedule I or II controlled substances. For many licensed cannabis retailers, effective federal tax burdens can become extraordinarily high because ordinary operating expenses remain non-deductible under Section 280E.

A retailer operating under an extraordinarily punitive effective tax burden has structurally less capacity to spend on platform services than one operating under a normal tax regime. The downstream strain is already visible in the Company’s own metrics: average monthly revenue per paying client declined from $3,029 in FY24 to $2,805 in FY25, and the Company itself ties that decline to spend compression in established markets amid continued industry stress.

That pressure also appears in receivables and credit quality, not just ARPU. The Company ended FY25 with net accounts receivable of $14.6 million, up from $10.1 million a year earlier, while the cash flow statement shows that FY25 operating cash flow was burdened by an $8.9 million increase in accounts receivable. FY25 also included a $4.4 million provision for credit losses, and the allowance for credit losses rose from $1.2 million to $4.2 million.

I do not treat that as proof that every dollar of receivables build reflects structural deterioration; the 10-K itself notes that 2024 benefited from a focused effort on collecting significant outstanding receivables, producing a higher-than-normal cash influx that did not recur in 2025. That stronger collections period also coincided with the quarter in which the co-founders made their initial $1.70 per share proposal. Standing alone, I do not treat that temporal overlap as proof of intent. It is, however, part of the relevant chronology.

Taken together, these figures are consistent with a customer base under real financial strain. If 280E relief improves retailer solvency, the benefits to Weedmaps should extend beyond marketing budgets to collections, bad-debt pressure, and broader customer health. Retailers retain more cash. That retained cash can support marketing budgets, platform subscriptions, and cleaner collections. Churn should stabilize, ARPU should have room to recover, and bad-debt pressure should ease. None of this requires Weedmaps to be a cannabis company. It requires Weedmaps’ customers to become healthier businesses.

Management itself struck a notably cautious tone on the 4Q25 call, and that caution should be acknowledged rather than waved away. The Company stated that Schedule III would not, by itself, unlock new monetization pathways, conventional e-commerce functionality, or broad strategic flexibility for Weedmaps in the near term, in part because exchange-listing and industry-structure constraints would remain. Management also suggested that some larger operators may already be realizing portions of the cash-flow benefit commonly associated with 280E relief through legal positions, consolidation strategies, or uncertain-tax-liability treatment. I do not dismiss those points. I treat them as reasons to model 280E relief conservatively and primarily through customer economics—not through an immediate transformation of Weedmaps’ own business model.

That same call also underscored that the near term remains messy, with management guiding first-quarter revenue down sequentially by a mid- to high-single-digit percentage. That’s a fair reason for the tape to stay skeptical in the short run. It’s not a fair reason to value the business as though the short run is all that matters.

Rescheduling’s timing is uncertain. But the 10-K itself now acknowledges that the December 18, 2025 Executive Order directed the Attorney General to complete the rulemaking in the most expeditious manner permitted under federal law, and the Company expressly notes that Schedule III would remove the Section 280E tax hindrance for cannabis businesses. As one observable input, prediction markets were pricing rescheduling at approximately 29–34% before July 2026, 61–65% before 2027, and 85% before 2028 as of my February 23 letter to the Board. As of March 12, 2026, the date the 10-K was filed, Kalshi prices for the same contracts were 32%, 64%, and 84%—broadly unchanged.

One legislative counter-risk should be acknowledged: a bill introduced this session would seek to preserve Section 280E for state cannabis businesses even under Schedule III rescheduling. I do not assign it zero probability. I do assign it low probability, particularly given the December 18, 2025 Executive Order directing DOJ to complete the rescheduling rulemaking on an expedited basis. Separately, there is public reporting suggesting the administration may be considering a broader review of federal marijuana policy beyond Schedule III, including potential descheduling. I have not modeled that outcome. If descheduling materializes, the valuation implications would be substantially larger than what any Schedule III scenario captures.

The correct response to that uncertainty is scenario modeling with disclosed assumptions, not omission. A valuation that treats rescheduling as zero-probability is not being conservative. It is baking in an assumption the public record does not support.

The other major variable is the federal hemp reset

This variable was not included in my prior letters to the Board because, frankly, the analytical basis for sizing it had not yet matured. Congress has now enacted a narrower federal hemp definition with an effective date of November 12, 2026, absent repeal, replacement, or further postponement. The Company’s own public disclosures have confirmed that intoxicating hemp products represent competitive pressure on the state-licensed cannabis ecosystem it serves. As that date approaches, this has become a required valuation input.

A proper valuation should also recognize the reverse implication: constraining that competing channel should return some portion of demand and spend to the licensed ecosystem rather than being treated as economically neutral. If intoxicating hemp has functioned as a competing channel siphoning off consumer demand and operator wallet share, then narrowing that channel should not be modeled only as an industry headwind on the way in and ignored as a partial anti-headwind on the way out. I do not treat that as a 2026 windfall. I do treat it as a legislatively fixed, non-zero, bounded benefit to the licensed ecosystem Weedmaps serves.

I am adding it to this analysis now because the record should be complete, not because it serves a narrative. The correct treatment is conservative and ramped: a gradual benefit through 2027 into 2028 and beyond, not a sudden 2026 step-change.

My base-case attribution is modest. I treat this as a bounded benefit to licensed-operator economics that should begin to matter more in 2027 and beyond. The Company’s own disclosures justify giving it non-zero weight, even if the per-share sizing remains my estimate.

With those variables in view, my standalone valuation framework

Before sailing through the cases, one framing point: my ~$2.75 per share intrinsic estimate is not the only anchor in this record. My February 9 letter formally established a $1.60–$1.80 Dutch Auction "Solvency Floor"—the range at which the Company could self-fund a compliant tender offer using less than half of available cash, instantly cure the Nasdaq deficiency, and do so at a valuation that brackets the founders’ own $1.70 proposal. That floor represents the minimum defensible capital allocation price, not the intrinsic value. The ~$2.75 estimate is the center of the standalone range that, in my view, a properly constructed public-information DCF supports. The gap between $1.60 and $2.75 is not ambiguity. It is the zone where a press-release "premium" gets built and where process integrity is the primary protection minority holders have.

The capital allocation question is not abstract. My February 12 letter documented ~$3.9 million in cumulative interest income forfeiture across FY2023 through 9M2025—the gap between what the Company actually captured on its idle cash and what the Effective Federal Funds Rate (EFFR) would have produced on the same balances with basic treasury management. FY2023’s implied yield of 0.11% is startlingly low against a 5.02% EFFR average, on ~$30 million in average cash. FY2024 fares just marginally better, 0.96% yield against 5.14% EFFR, on ~$44 million. That figure was sent certified mail to the Board, the Audit Committee Chair, and Baker Tilly.

It was not a rounding error. The ~$3.9 million total exceeds the Company’s reported net income for FY25. I received no response.

A board that let ~$3.9 million in risk-free yield evaporate over nearly three years, on a debt-free balance sheet, in a cash-flush Company, and then contemplates a reverse split instead of a buyback to cure a bid-price deficiency is not a board that has maximized the available option set. That documented governance record is part of the same analytical chain. It belongs here.

This is not presented as a banker’s model or as “the one true number.” It is a public-information-only range exercise designed to answer a simpler question:

Is the current stock price a fair representation of standalone value?

I believe the answer is no.

I am not getting to this range by assuming heroic terminal growth, an immediate 2026 step-change, or a sudden return to software-market multiple expansion. The framework assumes a conservative, ramped regulatory benefit and the bulk of value arriving through normalized 2028+ customer economics rather than near-term optics.

To keep the analysis disciplined, each case below is doing identifiable work. Each one reflects a view on the cash floor, the operating earnings power of the business, the timing and ramp of regulatory change, and how much of the value should be credited to normalized years rather than transitional noise.

The primary variable across these cases is not optimism versus pessimism. It is the timing and magnitude of the regulatory transition: how quickly 280E relief reaches the customer base and how effectively the hemp reset reroutes demand.

Bear case: prolonged status quo

Probability: 15%

In the bear case, federal reform drags, customer stress persists, and state-level compliance costs prove real. The market continues to apply a heavy discount because the Company remains trapped in deficiency-clock purgatory.

I still give the federal hemp reset some credit here — not because I expect a clean or immediate benefit, but because even in the bear case I do not think it should be modeled at zero. I assume implementation friction, workaround behavior, and a slower-than-hoped commercial re-routing back toward licensed operators, so the benefit remains modest and delayed.

Even in that draconian case, the valuation is not simply “cash and vibes.” If cash per share remains roughly where it was at year-end, a meaningful portion of the share price would still be supported by cash alone. On top of that, there remains residual operating value in a going concern with a known platform, an installed customer base, and optionality if conditions stabilize even modestly.

That is why I think ~$1.50 per share is a more defensible bear-case standalone value than the sort of sub-dollar level implied by recent trading, with only a modest portion of that value attributable to a conservative, ramped hemp-normalization benefit.

Base case: reform matters, but without heroics

Probability: 50%

This is the case I think the market still underweights.

A serious valuation cannot assign zero to federal reform effects, and it also cannot ignore that the federal government has now put a date on materially constraining intoxicating hemp products that compete with Weedmaps’ licensed-cannabis customers. I do not treat that as a 2026 windfall. I treat it as a partial 2027+ tailwind layered on top of a non-zero reform path.

Relief from today’s structural pressure on licensed operators can plausibly improve customer solvency, collections, churn, and marketing spend. The hemp reset can plausibly remove part of a federally tolerated competing channel that has siphoned demand and wallet share away from the state-licensed ecosystem. Because the real value of that improvement sits more in normalized years than in the immediate quarter, a proper valuation should capture more than transitional turbulence.

This is the scenario where the business is modeled carefully, but not punitively. The cash floor remains real. The operating value becomes easier to defend. The regulatory outlook is not treated as fantasy, but neither is it taken at face value without a ramp.

That combination is why my base case is ~$2.50 per share, of which I think ~$0.25 per share is attributable to a conservative, ramped hemp-normalization benefit.

Bull case: reform plus capital-allocation discipline

Probability: 35%

The upside case is not “to the moon.” It is the case where multiple things stop going wrong at once.

Federal reform arrives on a commercially relevant timeline. The board behaves like capital has an opportunity cost. Listing remediation gets handled without a value-destructive reverse split. And the late-2026 federal tightening of the hemp channel produces a more meaningful reversion of demand and marketing budgets toward state-licensed operators in 2027 and beyond.

Just as important, the market starts valuing MAPS less as a 2026 problem and more as a normalized micro-cap platform with a cleaner steady-state earnings bridge than the tape currently implies.

Nothing about this case requires magic. It simply requires investors to stop overweighting temporary dislocation and start giving real credit to normalized economics, cleaner cash conversion, and less distorted competitive conditions.

That gets me to ~$3.75 per share, with ~$0.50 per share of that value attributable to fuller — though still bounded — realization of the hemp-side tailwind.

The weighted math

Bear: 15% × $1.50 = $0.225

Base: 50% × $2.50 = $1.25

Bull: 35% × $3.75 = $1.3125

That yields a public-information-only intrinsic value estimate of roughly $2.79 per share. Call it about $2.75, and still safely north of $2.50.

And to be clear, one of the useful features of this framework is that it is not all blue-sky reform hope. By my rough sizing, approximately $0.32 per share of that weighted value comes from the now-enacted narrowing of the federal hemp loophole. That is a concrete anti-headwind the market does not appear to be adequately crediting.

Just as importantly, that conclusion does not require a reader to assume a heroic 2026 snapback. It requires only that temporary dislocation, affected trading, and bounded clean-up charges not be mistaken for permanent earnings-power destruction.

Could the exact number move with fuller access to the underlying projections, assumptions, and valuation materials? Of course. Up or down. That is precisely why the public record, however useful, is not the end of the exercise.

But on the public record alone, I think it is already enough to say this: a future “premium” bid anchored to an affected sub-dollar quote would not answer the valuation question. It would merely reframe it.

Why this matters in a future affiliated bid context

If an affiliated bid arrives, I fully expect the press release to emphasize premium.

Fine. Premium is a number. Value is the question.

A premium to a quote compressed by the Nasdaq deficiency clock, ownership-related bid deterrence, cannabis fatigue, a shrunken buyer universe, and transaction anticipation is not self-validating.

It may be good optics. It is not a substitute for a defensible valuation record.

The threshold question for any fairness analysis is not whether a bid represents a premium to where the stock trades today. It is whether the starting price itself reflects unaffected, uncoerced value. The public record already contains the ingredients to argue that it does not.

The Tax Receivable Agreement is a structural constraint on any market check

The TRA is also a required input here, not a footnote.

The founders’ December 2024 proposal stated that they beneficially owned ~32% of the common stock, had no intention to vote in favor of an alternative transaction, and believed a competing proposal was highly unlikely because a third-party buyer would face more than $100 million in incremental TRA cost at the offer price.

That’s not a clean auction backdrop. It’s a structurally deterred bidding environment. Any process that treats the absence of competing proposals as affirmative evidence of fairness—without first confronting the structural reasons for that absence—is missing a critical constraint.

For completeness, the 10-K confirms that estimated undiscounted future payments under the TRA could reach $138.9 million. The current recorded liability is only $2.7 million, reflecting the Company’s full valuation allowance posture and the fact that TRA payments arise only when actual tax benefits are realized. In other words, the headline number is a scenario ceiling, not a present cash burden. But it remains highly relevant to third-party buyer math, which is exactly the point the founders themselves made in December 2024. Symmetrically, the Company’s tax attributes represent a form of transaction-sensitive optionality that is not visible in the current tape.

In my February 12 letter, I separately asked whether a Rule 10b-18 open-market repurchase would trigger a TRA change-of-control event, since standard TRA definitions typically accelerate upon a transfer of control to an unrelated third party rather than a repurchase that consolidates existing control. I received no response.

The majority-of-the-minority vote, if used, must function as a real protection

In an affiliated take-private, a majority-of-the-minority condition can provide outside holders meaningful leverage over the outcome. But that protection depends entirely on how it is constructed. A vote measured by shares actually cast is materially easier to satisfy than one measured by disinterested shares outstanding. In a micro-cap with low institutional ownership, thin turnout, and a dual-class structure, that choice is not procedural trivia. It is part of the economics of the process, and if the Committee elects to rely on such a condition, it should disclose and defend that choice.

The Committee should also confront the structural context in which any minority vote would occur. The same capital structure and TRA dynamics that deter third-party bidders can also shape the practical composition of the unaffiliated voting pool. If the market check is constrained and the voting base is structurally thin, then a majority-of-the-minority vote cannot be treated as a substitute for rigorous valuation work. It is a protection only if it is designed and administered to function as one.

Why the public record now hits a wall

This is where the 10-K becomes both essential and insufficient.

Essential, because outside holders should not skip the public work.

Insufficient, because once that work is done, the unresolved questions are internal.

The filing confirms something more important than many readers may appreciate: management already ran a quantitative discounted-cash-flow-based goodwill test, concluded carrying value exceeded fair value, and recorded a $7.1 million goodwill impairment. Baker Tilly then elevated goodwill impairment to a critical audit matter because of the judgment embedded in forecasted revenue, cash flows, and discount rate assumptions. The public record therefore now proves the existence of an internal DCF framework while still withholding the inputs that would actually let outside holders evaluate it.

What did management actually project?

How did the committee and its advisors probability-weight regulatory timing?

Did they double count risk?

How did they treat settlement cash impact?

Did they analyze a tender or buyback against reverse-split optics?

Did they treat post-deficiency trading as affected?

How did they size the enacted federal hemp reset relative to the Company’s own prior disclosures about intoxicating hemp as a competitive threat?

Those are not public-file questions.

Those are board-room questions.

And that is why this post is not the end of the inquiry. It is the point at which the public inquiry reaches its limit.

My February 23, 2026 notice to the Board expressly requested written confirmation that the correspondence had been provided to the Committee’s financial advisors and included in the Committee record. No such confirmation was provided. Across three distinct substantive inquiries—treasury management practices, TRA interpretation, and routing confirmation—no response was received.

Bottom line

I waited for the 10-K because I wanted the freshest public data before saying any of this.

I have now done that work.

My conclusion is not that the public record proves a single precise fair value for MAPS in a future affiliated transaction. It does not. My conclusion is that the public record is now strong enough to reject superficial, tape-anchored valuation and to establish a credible standalone range materially above the affected quote.

That is a narrower claim than certainty. It is also the more serious one.

If a renewed affiliated bid arrives and asks holders to bless a price built on affected trading, selective conservatism, or premium optics untethered from intrinsic value, the question will not be whether the bid came with a headline premium. The question will be whether it clears the record that now exists. On current evidence, I do not believe a bid anchored to the tape would come close.

That is the point of building the record before the bid, not after it.

LEGAL DISCLAIMER

No Investment Advice: This post is for informational and educational purposes only. Nothing contained herein constitutes financial, legal, tax, or investment advice. The views expressed are the personal opinions of the author and should not be relied upon as the basis for any investment decision. As of the date of this publication, the author holds a long position in MAPS equity securities (including derivatives). The author’s interests are not necessarily aligned with yours, and the author stands to realize significant gains in the event that the price of the Company’s stock increases.

Right to Trade: The author may purchase additional shares or derivatives, or sell some or all of their shares (including closing or exercising derivative positions) at any time, for any reason, without further notice. The author disclaims any obligation to update the information contained herein or to notify readers of any changes to their position or market view.

Forward-Looking Statements: This post contains estimates, projections, and “forward-looking statements” that are based on the author’s independent analysis of publicly available information. These statements involve significant risks and uncertainties. Actual results may differ materially from the projections and there is no guarantee that the Company will achieve the values discussed. The author makes no representation or warranty as to the accuracy, completeness, or timeliness of the information presented.

Activism & Proxy Solicitation Safe Harbor Notice: This communication is provided strictly for informational purposes. Rod Alzmann is acting individually and not as a member of a “group” for the purposes of Section 13(d) of the Securities Exchange Act of 1934. The author does not have any agreement, arrangement, or understanding with any other person regarding the voting, acquisition, holding, or disposition of MAPS securities.

Not a Proxy Solicitation: This publication does not constitute a solicitation of a proxy, consent, or authorization. Rod Alzmann is not seeking proxy authority from any shareholder and will not accept proxy cards. To the extent this communication discusses how the author intends to vote his own shares or the reasons for doing so, it relies upon the exemption from the proxy rules provided by SEC Rule 14a-1(l)(2)(iv) and/or Rule 14a-2(b)(1). Shareholders must make their own independent decisions regarding how to vote their shares.

Analytical Tools: Portions of the analysis, frameworks, and visualizations in this post were developed with the assistance of AI analytical tools. All inputs, assumptions, editorial judgments, and conclusions are my own. The AI tool served as a research and drafting assistant; it did not independently generate investment recommendations or valuation conclusions. I make no representation as to the accuracy of AI-generated content and have reviewed all material for consistency with publicly available data. Any errors are mine.